The Tenant Credit Score Requirements NC Operators Use

We know tenant screening is the foundation of a profitable rental property. Rising living costs make this process trickier than it was even a year ago. The 2026 Triangle median rent sits right around $1,800, which puts extra pressure on household budgets.

Our team at Durham Elite Property Management reviews applications daily, giving us a clear view of these financial shifts. Let’s look at the data, what it actually tells us, and how to protect your investment. This guide outlines the specific tenant credit score requirements nc property managers rely on to minimize risk.

We see successful property managers clustering their qualification rules very tightly. A standard range falls between 620 and 660 for credit scores. RentPrep’s recent national data shows the average screened tenant has a score of 649.

Our standard practice requires a DTI of 40 to 55 percent, along with a zero-tolerance policy for prior evictions.

- Below this band, the risk of a tenant defaulting rises sharply.

- Above this range, the marginal benefit of a tighter floor does not justify the smaller applicant pool.

We analyze local data to keep our screening metrics perfectly calibrated. Recent reports from the North Carolina Judicial Branch show over 200,000 eviction filings statewide during a single 12-month period. This staggering volume proves why strict qualification rules matter.

Our experience shows that avoiding these costly legal battles starts with setting the right baseline numbers.

A single eviction gone wrong in Magistrate Small Claims Court easily costs an owner $4,000 in lost rent and legal fees. Consistent standards protect your cash flow from these heavy hits.

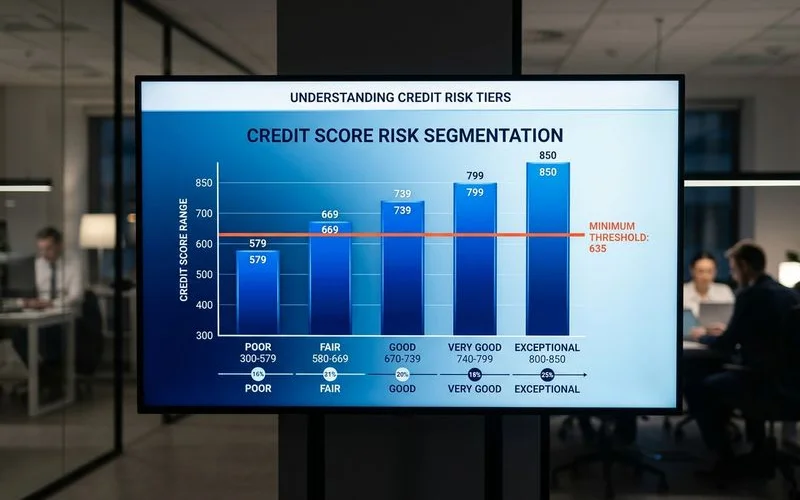

Why 635 Specifically

We picked 635 as the official threshold because it provides a reliable defense against default. After more than two decades of placing Triangle tenants, the screening data from thousands of applicants paints a very clear picture. The default-rate inflection sits right around the 630 to 640 mark.

Our records confirm this is the exact point where late-rent and eviction probabilities rise meaningfully. This 635 target is highly practical.

- A FICO score of 635 is easily verifiable through major bureaus like Equifax.

- We apply this number uniformly to every applicant to ensure total fair-housing compliance.

- Tighter thresholds above 700 shrink the applicant pool too aggressively for typical Triangle rentals.

- Looser rules below 620 carry a heavy risk.

Our screening process refuses to let default risk bleed into the management fee math through lost rent and property turns. A solid 635 score prevents those financial leaks. The data clearly supports holding firm on this specific number.

How DTI Works

We cap our rental DTI requirements at 55 percent for a very practical reason. Tenants above this threshold have almost zero buffer for sudden life events. A simple car repair or a surprise medical bill easily disrupts their monthly cash flow.

Our formula calculates total monthly debt plus proposed rent, then divides that figure by gross monthly income. If the ratio sits above 55 percent, the application faces immediate denial unless strong compensating factors apply. Below 55 percent, a tenant’s monthly cash flow can usually absorb minor financial shocks.

We use a standard mathematical approach to verify affordability. The table below illustrates a typical scenario for a prospective renter. This specific example highlights why looking at gross income alone is dangerous.

| Financial Item | Monthly Amount |

|---|---|

| Gross Monthly Income | $4,000 |

| Existing Car Loan | $400 |

| Student Loans | $250 |

| Credit Card Minimums | $150 |

| Proposed Rent | $1,500 |

| Total Debt + Rent | $2,300 |

Our final calculation divides the $2,300 total obligation by the $4,000 gross income. This results in a DTI of 57.5 percent. This specific applicant fails the baseline test.

We rely on these hard numbers to prevent emotional decision-making. A high consumer debt load is a major concern for 2026, making this calculation more critical than ever. Strict math eliminates the guesswork from the leasing process.

Compensating Factors

We do not run the screening process as a blind, rules-based filter. A borderline application occasionally holds hidden strengths, like a qualified co-signer, that mitigate the initial risk. Documenting these factors in writing alongside the screening file is legally mandatory.

Our strict documentation habits ensure complete defensibility if a decision faces a fair-housing challenge later. A few specific variables can rescue a borderline application. The right combination of these elements provides immense peace of mind.

- Qualified co-signer: A guarantor with their own 635+ credit score and stable income provides excellent backup.

- Larger deposit: Collecting a higher upfront sum, staying within North Carolina’s legal deposit limits, adds direct financial security.

- Long-tenure employment: Verifiable income stability, such as five or more years at the same employer, proves reliability.

- Strong prior-landlord references: Documented on-time rent history and clean lease compliance carry massive weight.

Our property managers carefully evaluate these items before making a final call. You must apply these exceptions uniformly across your entire portfolio. Inconsistent application of these rules leads straight to discrimination claims.

Thin-File Applicants

We frequently encounter young professionals and recent immigrants with limited US credit history. These thin-file applicants still need to meet the baseline standards. Recent data shows adults aged 20 to 29 only average a 662 credit score nationwide.

Our strategy places heavier weight on their compensating factors to offset the lack of a lengthy credit profile. The 635 floor technically still applies. Verifiable W-2 employment documentation becomes the primary focus for these individuals.

We also review documented international credit history where available.

A larger security deposit or a qualified co-signer often closes the gap. This balanced approach captures great tenants who just need time to build credit.

Zero-Tolerance Items

We enforce three strict categories that trigger an automatic denial regardless of the minimum credit score to rent nc. These are predictive behavioral markers, like prior evictions, not just soft signals. A past eviction is the single strongest indicator of a future lease violation.

Our internal screening data aligns perfectly with broader rental industry literature on this topic. Landlords face massive financial exposure if they ignore these warnings. You must protect your property from repeat offenders.

- Prior evictions: Any formal eviction action filed in the past seven years results in an immediate halt.

- Recent collections: Unresolved collection accounts exceeding $1,000 show a current inability to manage debt.

- Active charge-offs: Outstanding judgments indicate severe financial distress.

Our zero-tolerance policy protects owners from repeating another landlord’s nightmare. You simply cannot afford to gamble on an applicant carrying this level of documented risk. These hard stops exist for your financial protection.

Where This Fits in the Process

We place the 635, 55 percent, and zero-tolerance thresholds at steps two and three of our six-step screening pipeline. The remaining steps round out the picture by surfacing red flags a basic credit check completely misses. ID verification, criminal background checks, employment confirmation, and prior-landlord interviews complete the profile.

Our comprehensive process highlights exactly what credit score do landlords look for alongside behavioral indicators. You can compare these professional results directly against consumer-grade options. Read our detailed breakdown of Self-Screening vs Professional Tenant Screening to see what tools like TransUnion SmartMove lack.

We built this operational model to provide a massive advantage for local investors.

View our complete tenant placement service to learn how this system functions in the real world. Taking the right steps now saves you thousands of dollars later.

Our team is ready to help you implement these exact safeguards today. You need clear tenant credit score requirements nc guidelines to maximize your rental income. Contact us to discuss your property management strategy and protect your valuable assets.